A Beginner’s Guide to U.S. Health Insurance: What International Professionals and Founders Need to Know

If you’re relocating to the U.S. as an international founder, tech worker, or startup team member, navigating the American healthcare system can feel like deciphering an entirely new language. Unlike many countries with public healthcare systems, the U.S. operates primarily on a private insurance model and understanding how to protect your health (and your wallet) is essential from day one.

In this post, we’ll break down the basics of U.S. healthcare and answer the most frequently asked questions from visa holders, expats, and startup founders entering the American market.

🤔 Do I Need Health Insurance to Live in the U.S.?

Technically, you are not legally required to have health insurance to reside in the U.S. unless you're in a state like Massachusetts, California, or New Jersey, which have costly state penalties associated with not being insured. However, not having insurance can be financially devastating if you get sick or injured without coverage.

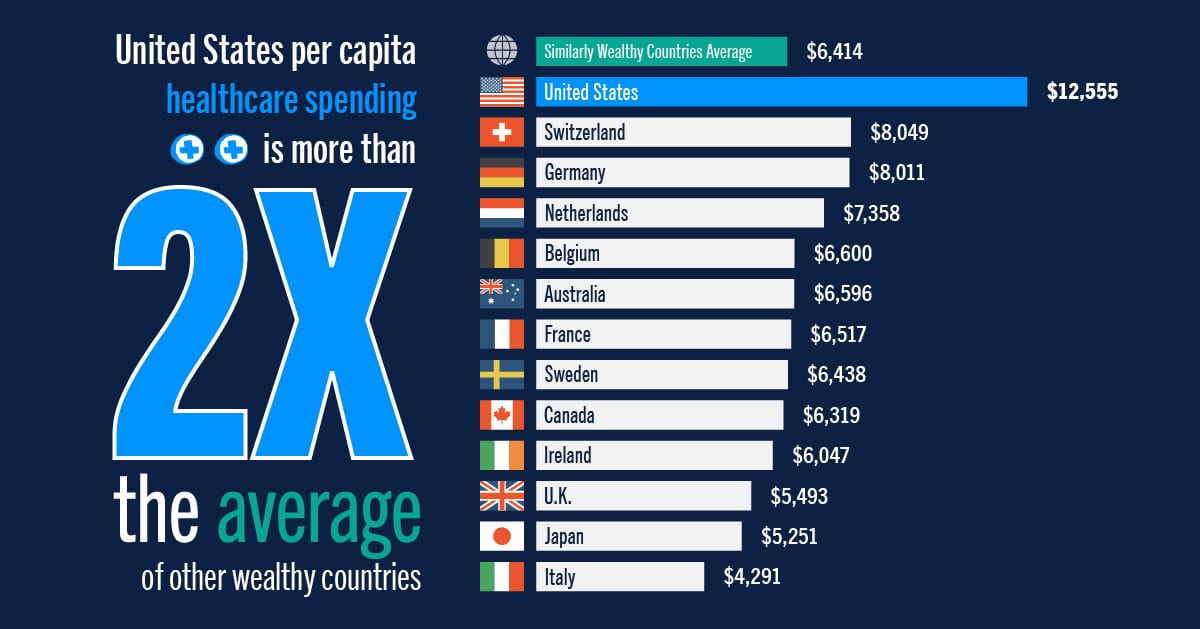

A simple emergency room visit can cost $2,000–$10,000+ without insurance, and even routine procedures can quickly become unaffordable.

If you're:

- On a visa (e.g., H-1B, L-1, O-1, E-2)

- A dependent of a visa holder

- Starting a business

…you absolutely should have coverage in place as soon as you arrive.

🏥 How Does U.S. Healthcare Work?

The U.S. system is insurance-driven and largely privatized. Here’s the simplified breakdown:

- Most people get insurance through their employer-sponsored plan.

- Others buy individual plans through the federal or state marketplaces such as Affordable Care Act (Obamacare) plans.

- Some may qualify for government programs like Medicaid (low-income) or Medicare (65+ or disabled).

- Health insurance gives you access to “in-network” providers doctors and hospitals that have agreed to negotiated rates.

- Without insurance, you’re responsible for 100% of the cost of care, often at much higher rates.

👤 What’s the Best Health Insurance for Visa Holders?

The best option depends on your visa type, employment status, and length of stay. Here are the main categories:

1. Employer-Sponsored Health Plans (Best Option if Available)

If your U.S. employer offers benefits, you’ll likely be eligible for a group health plan, which usually includes:

- Medical insurance

- Prescription drug coverage

- Vision and dental (sometimes optional)

- Mental health support

These plans offer better coverage at lower costs than individual plans, and are often partially subsidized by the employer

2. Individual ACA (Affordable Care Act) Plans

If you're self-employed, between jobs, or don’t have access to employer benefits, you can buy insurance via Healthcare.gov or your state exchange.

These plans are:

- Available to visa holders (even without a green card)

- Often more expensive than group plans

- Income-based subsidies may not apply to newcomers without U.S. income history

3. Short-Term or International Travel Insurance

If you’re only staying for a few months and don’t need full U.S. coverage, consider short-term health insurance or travel medical plans. But beware:

- These typically don’t cover pre-existing conditions

- May have very limited benefits

- Not suitable for long-term residents

💡 Tip: Startup founders can access group plans through a PEO (Professional Employer Organization) even with just 1–5 employees. In2America specializes in helping international teams access affordable group health insurance from day one.

💼 Is Health Insurance Included in Employment?

In many cases yes, especially for full-time W-2 employees. Most U.S. companies with more than 50 employees are required to provide “affordable” health insurance under the ACA.

Here's what you can typically expect:

- Employer covers 50–100% of the monthly premium (employer coverage varies for dependents)

- You pay the rest via payroll deduction

- You’ll have choices between different plan types (HMO, PPO, etc.)

- Coverage may begin immediately or after a 30- or 60-day waiting period

If you’re employed through a PEO (like In2America), you’ll often get Fortune 500-style benefits even if your startup is small.

🚨 Caution: Contractors (1099 workers) are not typically eligible for employer health plans. You’ll need to secure your own insurance.

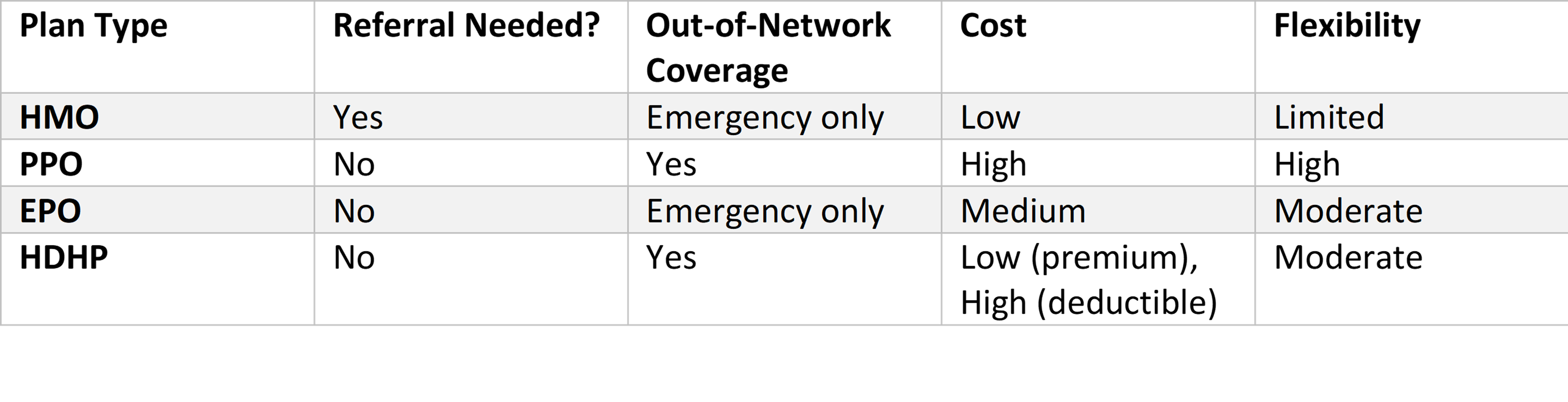

🧭 Understanding- U.S. Health Insurance Plan Types

When you enroll in a U.S. health insurance plan—either through an employer, the ACA marketplace, or a PEO you’ll typically choose from different plan “types.” Each type offers a different balance of flexibility, cost, and provider access.

Here are the four most common types:

1. HMO (Health Maintenance Organization)

- Lowest cost, most restrictions

- You must choose a Primary Care Physician (PCP) who coordinates your care

- Referrals required to see specialists

- No out-of-network coverage (unless it's an emergency)

- Typically offers lower premiums and deductibles

✅ Best for: People who want predictable costs and are okay with less provider flexibility.

2. PPO (Preferred Provider Organization)

- Most flexible option

- You can see any doctor, including specialists, without a referral

- Coverage for both in-network and out-of-network care

- Typically has higher premiums and deductibles

✅ Best for: People who want freedom to choose their own doctors and are willing to pay more for it.

3. EPO (Exclusive Provider Organization)

- A hybrid between HMO and PPO

- No need for referrals to see specialists

- No out-of-network coverage (except emergencies)

- Lower premiums than a PPO but less flexibility

✅ Best for: People who want some freedom without the high costs of a PPO.

4. HDHP (High Deductible Health Plan)

- Lower monthly premiums, but higher out-of-pocket costs

- Must pay a high deductible before insurance covers most services

- Often paired with a Health Savings Account (HSA) which allows pre-tax savings to be used for healthcare expenses

✅ Best for: Healthy individuals or families who rarely go to the doctor, aren’t on recurring prescription drugs, and want to save on premiums.

Quick Comparison Table:

🔍 Pro Tip for International Founders: Many employees in the U.S. are unfamiliar with these acronyms too. When offering health plans, educate your team on their options. If you’re using a PEO like In2America, you can get help explaining plan types and selecting the best mix for your team.

🔁 What Is COBRA Coverage?

COBRA stands for the Consolidated Omnibus Budget Reconciliation Act. It allows individuals who lose their job—or their health coverage due to quitting or being laid off—to continue their group health insurance for up to 18–36 months.

Key facts:

- Only applies to employees of companies with 20+ employees

- You pay 100% of the premium (plus a 2% admin fee)—this can be expensive!

- You must enroll within 60 days of losing coverage

- COBRA is often used as a temporary bridge between jobs

For visa holders, COBRA can help maintain health coverage while transitioning between employers or waiting for a new visa approval—but it’s not a long-term solution due to cost.

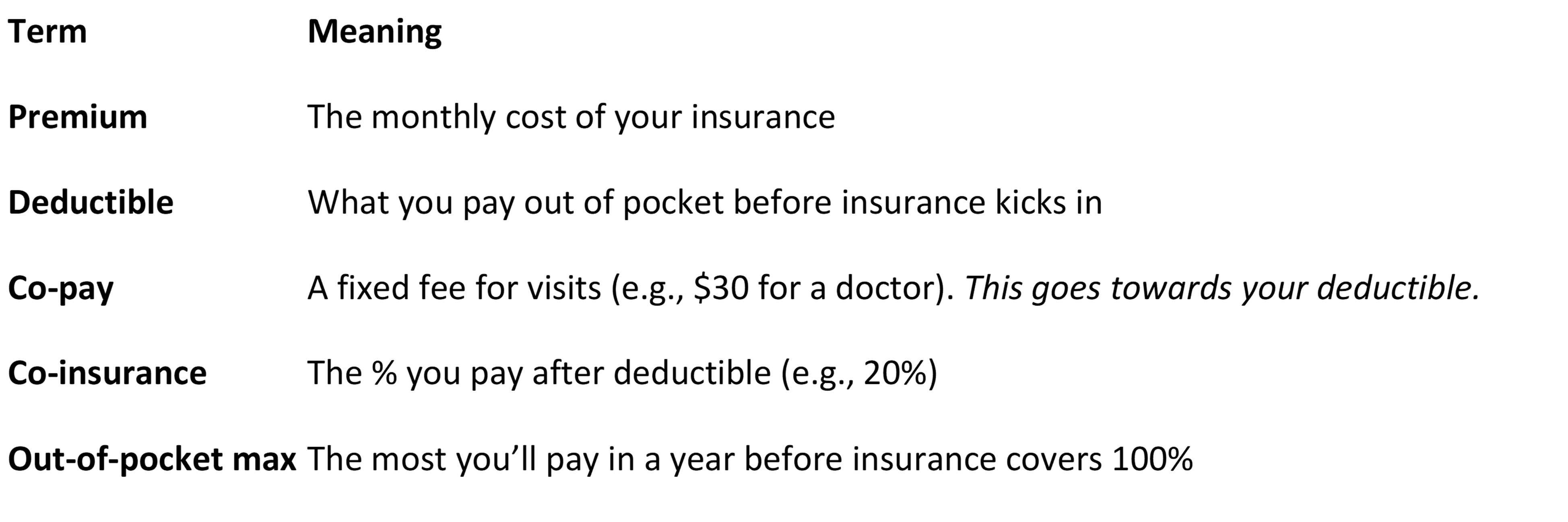

🧠Bonus: Key Terms You Should Know

🎯 Final Thoughts

Health insurance in the U.S. isn’t just a nice-to-have—it’s a critical safety net. For international founders, remote employees, and expats entering the U.S., the right insurance plan can be the difference between thriving and financial disaster.

If you’re launching a U.S. entity or building a small team, a PEO partner like In2America can provide access to elite benefits, handle compliance, and reduce your HR burden, with no minimum employee headcount required